wwing/iStock Unreleased via Getty Images

Back in early October of 2023, I wrote an article discussing the separation of the company that used to be known as Kellogg. Ultimately, the firm split up into two separate businesses. One of these is now known as WK Kellogg Co (KLG), which is the business that now serves as the North American cereal operations of the former conglomerate. The other enterprise to split off from this came to be known as Kellanova (NYSE:K). And it emphasizes the global snack operations, as well as certain key growth markets, of the brands that used to be owned by Kellogg.

In that article, I discussed why Kellanova made for an interesting opportunity for investors. Certain key brands that the business owns have been experiencing attractive growth. In addition to this, the global snack market is appealing in and of itself. Shares of the business, while not exactly cheap, were trading near the low end of the scale compared to similar firms. At the end of the day, this led me to rate the business a ‘buy’. In some respects, things have turned out quite well. Shares are up 16.2% since then. But relative to the broader market, the company has fallen short, as evidenced by the fact that the S&P 500 is up 26.1% over the same window of time.

As disappointing as this underperformance has been, the company is starting to show some real signs of progress. It still has plenty of room for improvement. But with management now looking to the future and looking for ways to capture additional value moving forward, and with shares still trading near the low end of the spectrum compared to comparable firms, I think that keeping the business rated a soft ‘buy’ only makes sense at this point in time.

Getting tastier

The purpose of this article is not to rehash the details of my October 2023 article. However, I do think a brief description of Kellanova and its operations is in order. Operationally speaking, the company is a truly global player, but its emphasis is on two primary types of products. Primarily, it focuses on catering to the global snacks market. Using data from the most recent quarter, about 63% of total revenue came from snack related products. Examples include Pringles, Cheez-It, Parati, and more. The rest of its revenue is split between international cereal operations, frozen foods, noodles, and other related products. All combined, around 80% of its revenue comes from either the global snacks space or all of its miscellaneous products that are sold to emerging markets. The beauty behind this kind of business model is that both the snacks market and pretty much anything to do with emerging markets should experience attractive growth compared to most other spaces in the food industry.

Author – SEC EDGAR Data

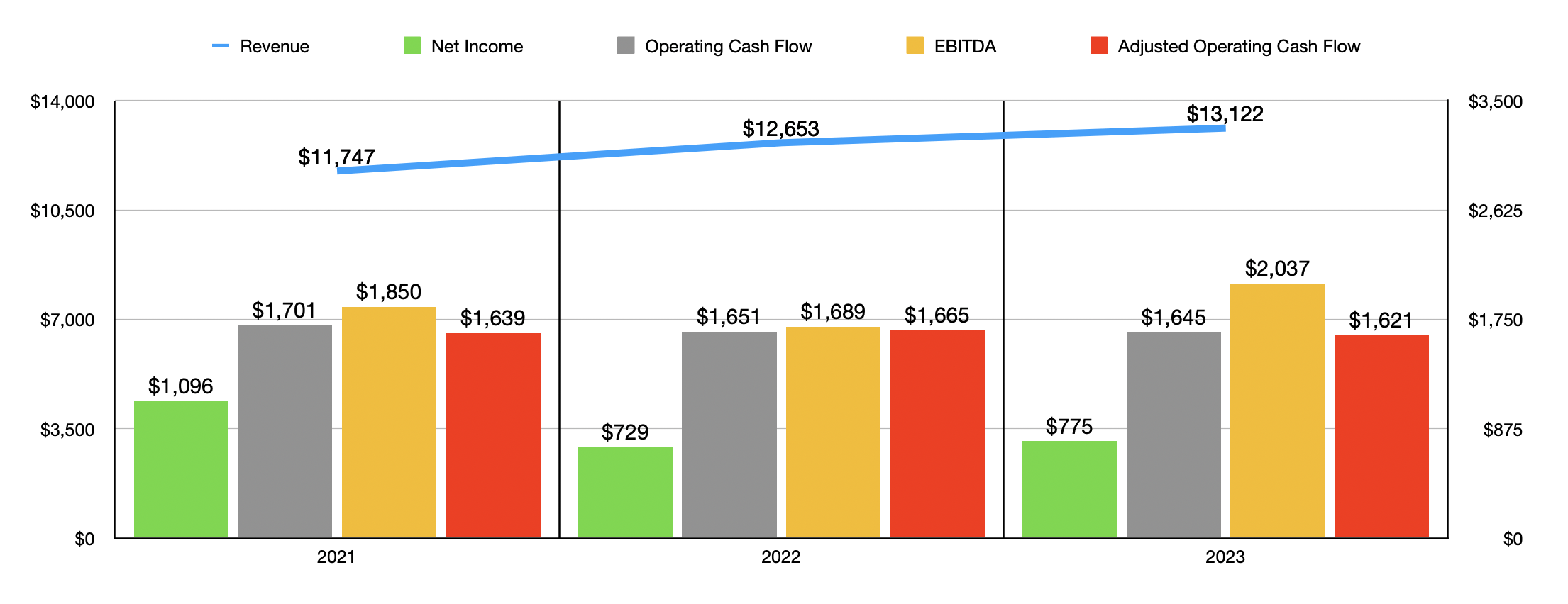

Over the past few years, management has seen some attractive growth on the top line. From 2021 to 2023, revenue achieved by Kellanova managed to grow from $11.75 billion to $13.12 billion. That’s an annualized increase of about 5.7%. Interestingly, revenue growth would have been even more impressive had it not been for foreign currency fluctuations. There would have been no change to sales back in 2021. However, on an organic basis, revenue for 2023 came in at $13.64 billion. That brings the annualized growth rate of the business up to about 7.7%. Much of this expansion seems to have come from the snacks market. In North America, for instance, organic snacks related sales jumped by 4.7% from 2022 to 2023. But in Europe, where the company gets about 16% of its revenue, snacks related sales skyrocketed by 17%. In Latin America, the company benefited from an organic growth rate in this category of 6.8%. And in the AMEA (Asia, Middle East, and Africa) regions, revenue jumped by 15.6%. This is not to say that the company didn’t benefit from other categories. In Latin America, for instance, organic cereal revenue shot up by 9.4%. And in the AMEA regions, organic sales popped higher by 24.4%.

As much as I wish I could say that profits and cash flows have followed a similar trajectory, that would not be a correct statement. Even if we strip out income from discontinued operations, we would have seen net income fall from $1.10 billion to $775 million over this window of time. To be perfectly fair, this is due in part to rising interest expense, but it’s also because of other miscellaneous income and expense items that have altered profitability over the years. If we look at just operating income, then we would have seen an increase from $1.38 billion to $1.51 billion during this window of time. Other profitability metrics have largely failed to impress. Operating cash flow fell from $1.70 billion to $1.65 billion. Even if we adjust for changes in working capital, we would have gotten a drop from $1.70 billion to $1.62 billion. The only real improvement came when looking at EBITDA. It managed to grow from $1.85 billion to $2.04 billion.

Author – SEC EDGAR Data

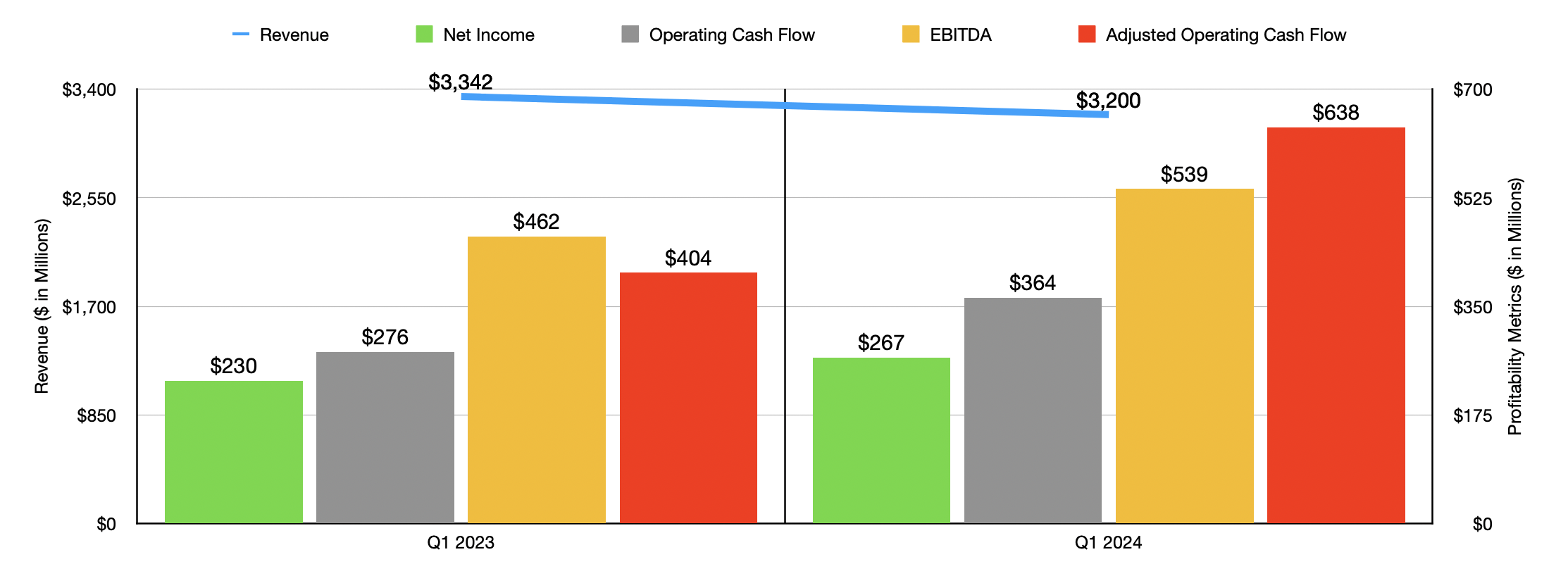

When we look at data covering the 2024 fiscal year, we only have results for the first quarter. And at first glance, this might seem uninspiring as well. Revenue for the company actually fell year over year, dropping from $3.34 billion to $3.20 billion. But even this requires some adjustments. If we adjust for a divestiture that the company made last year, the base would be slightly lower at $3.32 billion. And if we adjust for foreign currency fluctuations, sales this year would have been just under $3.50 billion. That’s an organic growth rate of 5.4% year over year. According to management, even as the volume of products declined, the firm benefited from an 8.5% increase attributable to a combination of pricing changes and changes in product mix.

On the bottom line, that is where we see the real improvements. Even though official revenue fell, profitability for the company improved, with net income climbing from $230 million to $267 million. This is after adjusting for the aforementioned discontinued operations. This is largely the result of an expansion of the company’s operating profit. According to the data provided, the company’s gross profit margin rose from 29.4% last year to 32.2% this year. If we use that disparity with the revenue achieved in the first quarter of 2024, that implies an extra pre-tax profit for shareholders of $89.6 million. This makes sense when you consider the impact that higher pricing typically has on low margin businesses.

On top of this, it’s worth noting that operating profits for the company would have been even higher had it not been for some other factors. Most notably, in the first quarter of this year, the company spent $101 million on network optimization activities. This is essentially restructuring operations following the spin-off in order to reduce costs in the long run. Instead of the 16.1% increase in profitability that I calculated, had the company been able to report the adjusted operating profit figures, we would have seen an operating profit rise of 29.5% year over year. Other profitability metrics for the company also improved. Operating cash flow, for starters, jumped from $276 million to $364 million. If we adjust for changes in working capital, we get a surge from $404 million to $638 million. And lastly, EBITDA for the business expanded from $462 million to $539 million.

Management expects organic revenue to grow by about 3% this year. So it does not appear as though the first quarter on its own will be the only time during which results for the company are better year over year. Adjusted profits per share are expected to come in at between $3.55 and $3.65. That’s above the $3.23 per share reported for 2023. This would imply adjusted income of about $1.24 billion. Management also said that operating cash flow should be around $1.7 billion this year. This should translate to EBITDA of somewhere around $2.14 billion.

Author – SEC EDGAR Data

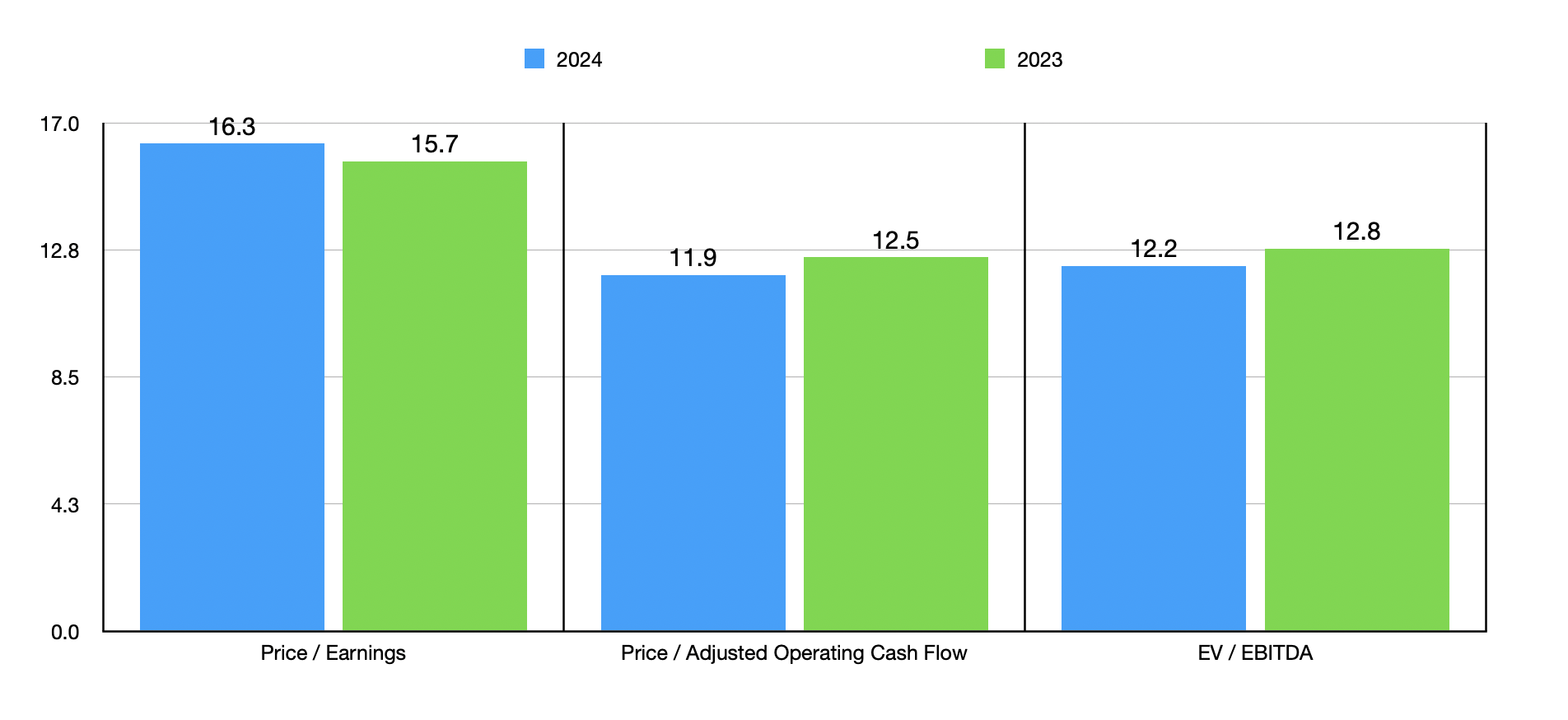

In the chart above, you can see how these estimates for 2024 and historical results for 2023 give some idea as to what the valuation of the company is. This is not exactly cheap, but for a high-quality food operator, this is appealing. In the table below, I then compared Kellanova to five similar firms. On a price to operating cash flow basis, two of the five were cheaper than it. But when it came to the other two profitability metrics, only one of the five companies was cheaper than our prospect.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Kellanova | 15.7 | 12.5 | 12.8 |

| Tyson Foods (TSN) | 54.9 | 9.1 | 23.6 |

| McCormick & Company (MKC) | 26.4 | 14.7 | 18.2 |

| Hormel Foods (HRL) | 21.9 | 13.2 | 14.5 |

| Conagra Brands (CAG) | 14.7 | 7.7 | 12.2 |

| Mondelez International (MDLZ) | 21.5 | 18.8 | 13.4 |

Before I wrap up this article, I would like to touch briefly on what other sources think of Kellanova. In the image below, you can see the rating of the stock according to not only the analysts that write for Seeking Alpha and Wall Street analysts, but also for the Quant Rating system that Seeking Alpha has established. Compared to other players, the overall assessment of Kellanova is decent, but far from great. Certainly, the leader of the pack would be Mondelez International, followed by Tyson Foods. Kellanova, meanwhile, would be tied with McCormick & Company and Conagra Brands in third place.

Seeking Alpha

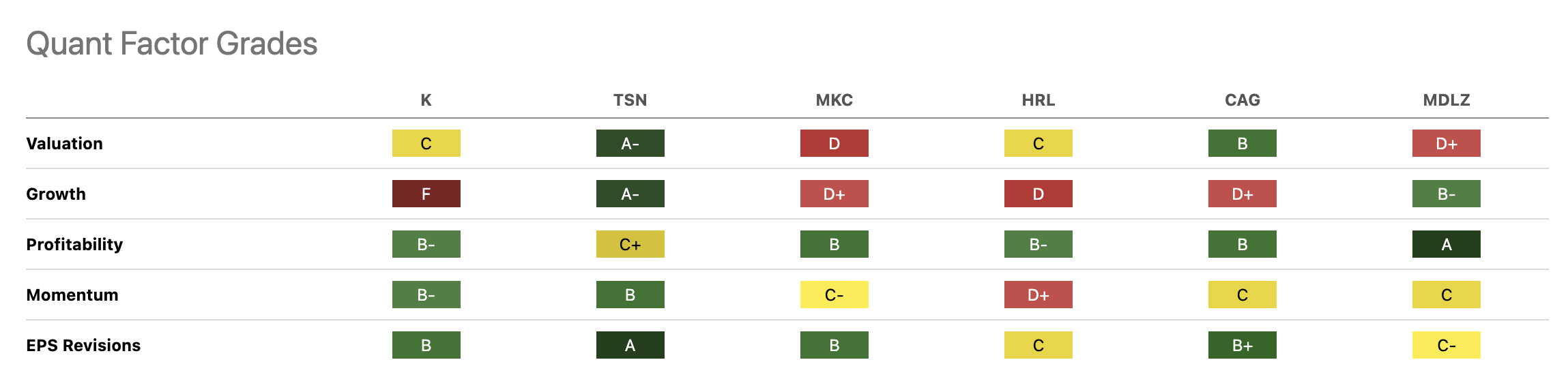

In the next image below, you can see how different aspects of the company are weighted by the Quant Rating system. On valuation, the company is decent, but not great. And it’s actually quite good when it involves profitability, momentum, and EPS revisions. But where it really shows up weak is on the growth side of things. If it weren’t for that, it looks as though only Tyson Foods would be rated higher than Kellanova currently is. As I demonstrated, however, you have to dig under the hood for this growth. Actual organic revenue has been overshadowed by foreign currency fluctuations and other factors. When you adjust for this, you see that growth for the company is quite solid. This is especially true on the bottom line, with profit figures growing at double-digit rates.

Seeking Alpha

Takeaway

From what I can tell, Kellanova is doing a pretty good job at this point in time. Is there room for improvement? Most certainly there is. But with how shares are priced compared to similar firms and how well the company is doing when you remove all of the noise, I think that a soft ‘buy’ rating is perfectly logical at this point in time.

{kind=link}