Richard Drury

I’ve had a lot of time to think about this. And I’ve alluded to it many times here. And now that it is up and running, fully-invested and operational, what I refer to as my Yield At a Reasonable Price (YARP) dividend stock portfolio, which contains a significant portion of my liquid net worth, is what I aim to be the top driver of my retirement lifestyle, financially speaking.

Defense wins championships. It also saves retirements. I am semi-retired or “micro-retired” as I like to say, since I work as much now as ever, albeit on my own schedule. And the past couple of years have convinced me of two things: writing for Seeking Alpha is great, and my YARP portfolio, which combines active pursuit of dividend income, “tail risk” protection against major market drops, and upside through dividend stocks, ETFs and index call options is the total portfolio approach I’m going to prioritize for my own money, hopefully for decades, as my 60th birthday arrives this week.

Why not just follow one of the existing, traditional dividend stock approaches?

Most dividend investors are familiar with and understand the basic mission of strategies like dividend growth, owning higher-yielding stocks of quality, dividend aristocrats, and others. These are deservingly popular due to their past success. But that’s the past.

I think modern markets have changed so significantly, I’ve decided that for my own retirement sustenance and stability, I am borrowing what I think are the best parts of traditional dividend stock strategies, and adding some features that I’ve used for decades in my own work.

Since absolutely no one knows the future, should we just hang in there, invest in unhedged stock-heavy portfolio allocations like many in my Baby Boomer generation and the Generation X folks do? And should “defense” be defined solely as some bonds and cash? My answer to both those questions is a resounding NO.

I’d never call someone out for committing to one of those mainstream approaches, and they each have some advantages over what I’m doing via my YARP portfolio approach. There are tradeoffs galore between YARP and traditional dividend strategies, especially for taxable accounts. So every investor needs to make their own decisions. I’ve made mine, and I’m putting it out there now, as I’ve just completed my initial set of 40 stocks that I tactically manage.

Investing is a serial learning experience. I started this article with that background because while I feel that the YARP portfolio approach may appeal to a wide range of investors, I designed it based on managing “other people’s money” for nearly 30 years, as a fiduciary to those families, then transitioning (when we sold the practice) to research, writing and, as noted above, a more intense focus on my own money. After being the least important client in my business, now I’m the only one!

The goals of a YARP portfolio are simple:

1. Identify fundamentally sound businesses (stocks)

Sustainable profitability is the first thing I look for. That does not mean these companies don’t have issues. In fact, buying “ugly” stocks is often where the best returns come from, since investors get caught up in the moment when a prominent stock slides, and they forget about the cash flow machine it represents, which can allow it to weather storms that companies with systemically weak fundamentals cannot.

2. Grab as much dividend as I can

Every calendar quarter is a new set of circumstances. I have 40 stocks, they all go ex-dividend during each quarter, announce earnings during each quarter, have company news, industry news, macro and supply and demand factors that influence their stock prices during each 3-month period. This creates opportunity for those like me who are willing to be more nimble when necessary, and who are OK trading off lower tax-efficiency with the goal of earning a much higher income from their portfolio and potentially a higher total return as well.

3. Methodically rotate stock weights using the YARP factor and technical analysis

Most dividend investors ignore a lot of that interim price movement. But I’ve been a chartist since 1980, and I developed the YARP factor as a statistic to analyze dividend stocks during the last decade. So I add those to the mix, and am willing to be very tactical and active if and when needed, all in the name of maximizing total return and avoiding big losses.

4. Add a pair of “wings” to the strategy using call and put options on major market indexes

The puts provide the tail risk, the calls aim to enhance the return when either the entire stock market is on a roll, or when as we’ve seen frequently in recent years, stocks with above-average yields drastically underperform the S&P 500 and Nasdaq 100 indexes.

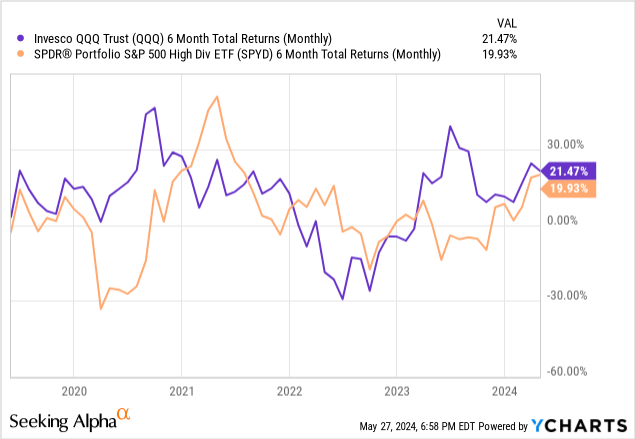

As a simple example, here is an ETF that tracks the 80 highest yielding stocks within the S&P 500, versus the very non-dividend-oriented Invesco QQQ Trust (QQQ). These two have a very cyclical relationship, and there have and likely will be times when QQQ-like investing is the “only game in town” for total return. I am not a homerun hitter, but more of a high batting average type if you will. I want to be competitive as often as possible, without taking on a ton of risk. So call options on S&P 500-type indexes and ETFs, or those on QQQ or similar will typically be part of the YARP portfolio, albeit a small portion. The main event here is dividend income and price appreciation from those 40 stocks.

My portfolio is built. Now, it is all about managing it. NOT about leaving it alone.

It is quite a process, and it’s a continuous one. Building a stock portfolio is easy if you want to do so without much thought, research or discipline. Many newer investors appear to just own what they “think” they should own, based on what everyone else talks about owning. That works until it doesn’t.

Don’t lose big

The overriding mission for me is that headline immediately above. I’ll give up dividend income and price appreciation any time, if it means I am greatly lowering the risk of losing big.

I am a long-term investor. However, I firmly believe that in this post-pandemic market climate, one of the most dangerous things an investor can do is rely on the “time in the market” or “I’m a long-term investor” mantra that simply does not work the way it used to. Maybe if you have 20-40 years to build wealth.

But if that wealth has already built, risk-management is priority number 1, 2, 3 and 4. That’s what governs my approach. So, while I like the long-term potential of equity investing, the last thing I’m going to do is fall in love with these inanimate objects, stocks, that do not care what happens to me and my family.

2 must-have elements of this approach

As such, I manage my equity portfolio with two non-negotiable features:

- Always have some form of “tail risk” hedge, and

- Be willing to adjust the portfolio weights of any position, at any time

Stock position sizing in the YARP dividend portfolio

Those positions will each have a weighting of 1% to 5% at any time. That allows me to focus less on whether to sell out of something or buy something new. I think way too many investors focus too much on when to buy a “whole” position in a stock or when to sell it all. I have always felt more comfortable managing money as a systematic process based on the relative attractiveness of a group of securities. Markets are such that these days, and I think going forward, most investments in stocks and ETFs are “rentals” and not buy and hold forever. At least for me they are.

By “rental” I mean that while I’d always love to hold a stock for years, that is not compatible with wanting to “avoid big losses” which is rule number one for me. So to “own” stocks to me means to identify a set of businesses that have the characteristics I look for, that convince me I can own at least a 1% position for longer than a year, hopefully several years.

YARP investing: the key difference (to me)

But where my approach differs from any other I’ve seen is in the rotation of position sizes. At any point in time, any of the 40 stocks can be 1%, 5% or some round number percentage in between. Never less than 1% in each of the 40 stocks, and never more than 5% (at cost) in any of those stocks. This creates guardrails, and put the emphasis on pursuing as much dividend income as I can, balancing that with avoiding ugly chart patterns and being too greedy.

I will change the 40 stocks, but not routinely. The way markets work today, most stocks will have up and down moves of double-digit percentages nearly every year. So, I’d rather get to know 40 companies well, and use my decades of charting experience and risk management techniques to produce alpha.

There are times when most of the 40 look great, and I have to limit some positions because 40 stocks at 5% is 200% and I only have maybe 90% of the portfolio to work with. So I consider 2-3% to be a “neutral” position per stock. The closer a stock gets to its ex-dividend date and the better it looks technically, the higher the weighting. The closer it gets to earnings, the further it is from the ex-dividend date, and the worse it looks chart-wise, the lower the weighting. There are other factors, but those are the key ones at a high level.

Earnings: my least favorite season

Why do I consider a stock approaching earnings to be less attractive? Have you seen what happens to stocks that miss earnings these days? It is not like “the old days” because now, earnings have become like a sporting event. I am about making money quietly, not trying to speculate on events. And, stocks often rise into earnings, so reducing the position a bit when I’m already profitable is part of the balancing act for me.

This is why I often state in my articles that my version of a “buy, sell or hold” rating is different from the norm. A lot of what I do is. My investment process simply does not jive with the idea that I am “in” or “out.” I am always both.

I also own SPY puts and calls, out of the money, which allow me to get that tail risk protection (from the put options) alongside a relatively large cash position, yet also have some inexpensive exposure (the call options) should this current market malaise turn out like many others, and QQQ and SPY return to “escape velocity” and run up more, continuing this historic recent run in the largest stocks.

What I look for in choosing the 40 stocks

I consider ANYTHING I think can make me money in the way I aim to: no big drawdowns along the way, businesses I can understand, anywhere on the globe. So I’m agnostic to all of it, but the “core” is more large cap. Smaller stocks are eligible, but I’m just not finding many that are both high yield and what I consider high quality. I’m more likely to “ETF” that unless/until I run out of good ideas in the large cap.

I prioritize price analysis/technicals, and I am a contrarian at heart. Looking back at some of the recent articles I wrote about stocks as I built the portfolio the past few months, it is fair to say that several were stocks that looked tarnished at the time, but have since lifted off. I refer to this as a total return “trifecta”: decent dividend yield, ex-date approaching, upside in the stock price.

Here’s a summary checklist of the qualities I tend to look for, fundamentally-speaking. This has been a rigorous process of screening, filtering, reading company analysis, and making extensive use of the Seeking Alpha quant ratings, particularly the Profitability rating. Frankly, as much as I respect the other ratings (valuation, momentum, etc.) since I am only trying to get 40 good businesses.

1. Seeking Alpha Profitability Grade of at least B (among other valuation measures and inputs from a wide range of sources I used, including but not limited to the vast amount of data and analysis from Seeking Alpha). I am not a fundamental analyst, but I’ve been around the stock market long enough to have a strong feel for what has worked for me over the decades.

2. Dividend yield of at least 2% above the S&P 500 for most or all of the 40 positions. Ideally, I’d find 40 stocks I like yielding 4% or more, and own them all. Guess what? Not possible for me in this environment. But at a time when the S&P 500 yields only 1.3%, getting 2-3% above that (3.3%-4.3%) is about all I can expect without truly “reaching for yield.”

The above chart shows how historically difficult it is for yield stocks in general. The S&P 500 has rarely had a yield this low since the SPDR S&P 500 Trust ETF (SPY) was introduced 30 years ago. It touched just below the current 1.27% mark for a few weeks in 2021 after some stocks cut their dividends during the onset of the pandemic. Other than that, a dip near that area during the dot-com bubble is all there is on this chart. Other than that, we have to go back to the last century.

So I do feel that there’s a good chance that the S&P 500 yield will rise as part of a market correction, and that will prompt some good YARP stocks getting sold off to the point where I can add them to the portfolio at yields closer to 4% or higher. To be clear, I don’t need that to happen. And I don’t know when it will happen. I just do feel strongly that it will happen in the foreseeable future.

3. A dividend payment I consider to be above-average in terms of safety (based on sources I follow, and my own judgement). Again, I am not buying and holding the stocks, and by trying to increase the weightings of stocks to qualify for more yield when they go ex-dividend each quarter, the annual yield is less important than the ability for me to create a total return over time with low drawdowns.

4. A long-term price pattern that is at least “workable” for me as a tenured technician.

That typically means that the stocks I choose will not be at or near all-time highs, as that likely means their yields are too low to qualify for the portfolio. And I like being a contrarian about this, since markets today appear to be very willing to embrace a stock after it has fallen in a panic, and been forgotten about for a while. This is not “buy the dip,” but more like, “see the dip, stash it in my watchlist and when the yield and technicals align and the profitability is still OK, consider it then.”

Why not simply use the same popular metrics everyone else uses?

I happen to be in the minority of investors who do not put a high priority on traditional valuation metrics. As I see it, stocks rarely trade near their “fair value” and popular approaches that include forecasting earnings and sales, and making long-term macro calls make an investor sound smart. But at the end of the day, there’s only one thing that matters: do the prices of the stocks I own go up during the time I own them. Like I said, this is not traditional. It is just what I believe in, and it represents a sum total of decades of trial and error. Yeah, lots of error! If they are not ideal on, say, valuation, I can stash them as 1% positions and look for a time to up that weighting. This has been a big key to my recent performance, in which Utilities suddenly came to life, as well as REITs. I own a lot of stocks in those two sectors, but since I can vary the position sizes tactically as I wish, I was able to capture the surge in those groups, get some dividend yield along the way, then downside the positions a bit as they start to appear “tired” technically.

The 40 stocks in my current portfolio

Here are the stocks. The weightings are proprietary, as it is what makes the strategy go. And those weightings are adjusted frequently at times, especially when a lot of these stocks are approaching ex-dividend dates and earnings release dates.

Notice that the Seeking Alpha Profitability Grades for these stocks all meet the “B or better” criteria I established. But valuation and growth are a mixed bag, for reasons explained above.

29 of the 40 stocks yield at least 3.3%, or at least 2% above the S&P 500’s trailing dividend yield. I’d like to get that number up, but not by buying companies I judge to be of questionable corporate strength.

| Seeking Alpha Quant Grades | |||||

| Symbol | Stock Name | Valuation | Growth | Profitability | Ex-Dividend Date |

| AMCR | AMCOR PLC F | B | D+ | B | 5/21/2024 |

| AMT | AMERN TOWER CORP REIT | D- | B | A | 6/14/2024 |

| AVB | AVALONBAY CMNTYS INC REIT | D | B | A | 6/28/2024 |

| CAG | CONAGRA BRANDS INC | B+ | D+ | B | 4/29/2024 |

| COP | CONOCOPHILLIPS | D | D+ | A+ | 5/10/2024 |

| CPB | CAMPBELL SOUP CO | C | D- | B- | 7/3/2024 |

| CPT | CAMDEN PROPERTY TR REIT | D | B+ | B+ | 3/28/2024 |

| CSCO | CISCO SYSTEMS INC | B- | F | A+ | 7/5/2024 |

| CVS | CVS HEALTH CORP | A+ | D- | A+ | 4/19/2024 |

| CVX | CHEVRON CORP | C- | D+ | A+ | 5/16/2024 |

| DGX | DOW INC | D- | D | A | 7/8/2024 |

| DOW | DUKE ENERGY CORP | B | D+ | A | 5/31/2024 |

| DUK | CONSOLIDATED EDISON | C+ | D+ | A+ | 5/16/2024 |

| ED | EQUITY RESIDENTIAL REIT | C- | D | B- | 5/14/2024 |

| ESS | ESSEX PROPERTY TR REIT | D | B | A- | 6/28/2024 |

| ETR | ENTERGY CORP | B | D+ | B+ | 5/1/2024 |

| EXR | EXTRA SPACE STORAGE REIT | C | A | B+ | 3/14/2024 |

| GLW | CORNING INC | C- | C- | B | 5/31/2024 |

| HD | HOME DEPOT INC | D | D- | A+ | 5/30/2024 |

| HPQ | HP INC. | A | F | A | 6/12/2024 |

| HSY | HERSHEY CO | D+ | C+ | B+ | 5/16/2024 |

| IP | INTERNTNL PAPER | C- | D | B | 5/23/2024 |

| JNJ | JOHNSON & JOHNSON | D | D+ | A+ | 5/20/2024 |

| KMB | KIMBERLY CLARK CORP | C- | D | A | 6/7/2024 |

| KMI | KINDER MORGAN INC | C | D+ | B+ | 4/29/2024 |

| KO | THE COCA-COLA CO | D | D+ | A+ | 6/14/2024 |

| LMT | LOCKHEED MARTIN CORP | C | D- | A+ | 6/3/2024 |

| LYB | LYONDELLBASEL INDS | A- | D | A | 6/10/2024 |

| MMM | 3M CO | A- | F | A+ | 5/23/2024 |

| NEE | NEXTERA ENERGY INC | D | B+ | A- | 6/3/2024 |

| PAYX | PAYCHEX INC | C- | C- | A+ | 5/9/2024 |

| PEG | PUB SVC ENTERPISE GP | D | C- | B | 6/7/2024 |

| PFE | PFIZER INC | A | C- | A+ | 5/9/2024 |

| PRU | PRUDENTIAL FINL | C | C+ | A+ | 5/20/2024 |

| RTX | RTX CORP | D+ | C- | A+ | 5/16/2024 |

| SBUX | STARBUCKS CORP | D | C+ | A+ | 5/16/2024 |

| SNY | SANOFI ADR | C+ | D | A+ | 5/9/2024 |

| TROW | T ROWE PRICE GROUP | C- | C+ | A- | 6/14/2024 |

| TXN | TEXAS INSTRUMENTS | D+ | D- | A | 5/7/2024 |

| VZ | VERIZON COMMUNICATN | B+ | D- | A+ | 4/9/2024 |

“Long term buy” is a term I define differently. Blame modern markets.

I want to own 40 good stocks, but not at the same weightings throughout the holding period. My reasons are strongly rooted in my own experience in the stock market, and seeing it evolve since the 1980s

Today, markets are influenced by algorithmic trading, indexation, and piles of government and consumer debt. Those are risks that make me an automatic “renter” of most things, not a buyer, until the system “clears” from those years of excesses. I have no idea when that will be. In the meantime, my only long-term holdings are T-Bill ETFs.

One of my core principles: the stock market is just a tool, a means to an end

I think investors too often believe that the stock market is something that is inherently not risky to their wealth building efforts if they give it enough time. That’s not the case historically.

There have been lost decades and lost periods of 20 years, typically after excesses like we’ve seen in recent years (debt buildup, leverage at the consumer and government levels, etc.). To me that means I am investing for growth and income as I always do, but I am so much more prepared for worst-case scenarios like what we experienced my second year in the business (1987).

Those life-changing events are not something any of us should count on, just as we don’t count on only living a very short life if we are healthy. But we still buy life insurance. And car insurance in case of an accident. I like to have a similar element in my portfolio, and I think covered call ETFs make people think their downside is protected. It is not as protected as they think, unless they take an additional step to protect it.

For me, it is put options, inverse ETFs, higher than normal T-bill allocation – usually a rotating combination of all three. Those additional market tools are simply a way to add some guardrails around the main stock portfolio. Because even if I thought the whole market looked awful, I’m still committing to having 40% of the YARP portfolio invested in stocks (40 stocks, 1% minimum weight each). So I can use those other tools to hedge or even exploit extended major market downturns.

I invested through three years of market declines (dot com bubble) and the 18-month crisis from 2007-2009. That and other major market drops are what formed the risk-managed nature of everything I’m describing here. Bottom line: a portfolio of high-quality stocks is not what it used to be, so if my goal is to produce strong income and avoid big loss, it will take more than just owning stocks.

I hope YARP will be a completely unique way for investors to pursue above-average dividend income and protection of capital, while still retaining virtually uncapped upside. In laying it out in this level of detail philosophically, I hope that others will benefit from it. But I’m realistic. Just because it works for me, that doesn’t mean anyone else will see the value in it that I do.

My YARP portfolio: final thoughts for now

Like I always say, everyone can play offense… and anyone can pick a stock or fund with a very high dividend yield and buy it. But few have really learned how to play responsible, sustainable defense. That has always been what I think has separated me from the crowd as a portfolio builder, even if it cost me a few clients over the years because I was not “aggressive” enough. Like I said, anyone can play offense, that’s the easy part. But what I built a career on was the other side, the one that folks tend to only remember how important it is when markets fall quickly. Because by then, it is too late to start preparing.

Fluctuating those position weightings, if I do it well, can double the dividend yield and limit losses quite a bit. That’s my key to generating lower stress total return. And once we get to a period where tech doesn’t dominate everything else, I think this is an S&P 500-beater over the next decade. That’s my aim anyway.

I’m not into “static” portfolios. I think the days of getting sustained high total returns with any consistency from most stocks are done for a while. For me, that means replacing that with a more dynamic allocation, aimed at capturing more dividends in dollars from the same stocks, rather than just sitting back and collecting 40 payments every three months. I’ll look forward to all feedback on it.

{kind=link}